In the last 24 hours, the U.S. announced a temporary suspension of high tariffs on imports from China, granting a 90-day relief period for goods that have been facing significant cost barriers.

Under this agreement, U.S. tariffs on Chinese imports were reduced from 145% to 30%, and Chinese tariffs on U.S. goods were lowered from 125% to 10%. This agreement does not affect the tariffs imposed under the elimination of the de minimis exemption; this policy, enacted through an executive order, removes the duty-free treatment for low-value imports (under $800) from China and Hong Kong. As a result, these shipments are now subject to a 120% tariff, effective May 2, 2025. This move aims to close loopholes that allowed certain goods to enter the U.S. market without tariffs, thereby impacting Chinese-owned marketplaces such as Shein, Temu, and others that relied on this exemption.

This move is poised to shake up the DTC landscape, particularly for brands in the clothing and apparel, CPG, and durables sectors. With this sudden change, brands that have been holding back on making any inventory investments due to the cost burden of tariffs are now faced with a critical decision to make: how much inventory should I order?

With tariffs temporarily lifted, many brands are now better positioned to place orders they had deferred due to high import costs. And while the reduced tariffs are a massive relief to brands with Chinese manufacturing exposure, this sudden influx of demand could create a different ripple effect across the supply chain.

Brands that were previously cautious about their inventory PO sizing—and minimizing their days or weeks of coverage—are now likely to rush to secure goods while the suspension is in place, leading to a potential surge in orders.

This demand spike isn’t just a possibility—it’s a likely scenario given how many companies have been putting off new inventory orders due to the recent tariff environment.

As brands rush to take advantage of the tariff suspension, the immediate consequence could be a significant surge in demand for freight space. This increase in demand could create a supply shock, driving up freight costs as shipping lanes and container availability get squeezed. This scenario mirrors what we saw during the COVID-19 pandemic, where sudden disruptions led to skyrocketing freight prices and capacity constraints.

So the key question here is: will the net benefit of reduced tariffs outweigh the increase in freight costs? If shipping costs spike significantly, the overall savings from the tariff suspension could be diminished, leaving brands in a precarious position.

Consumer brands need inventory, period. However, in a scenario where all the pent up demand from brands deferring POs comes rushing in all at once, we may not see the cost burden come down as much as some may think; rather, we'll see a displacement in cost, where the tariff burden may be lower, but the overall landed costs net of everything still elevated.

In light of the tariff suspension, brands need to rethink their inventory strategies. An 80/20 approach, where brands focus on their top-performing "hero" products, is crucial. This means prioritizing inventory that has the highest turnover and profit margins, ensuring they can meet consumer demand without overextending financially.

At the same time, this is an opportunity for brands to right-size their catalogs. Liquidating slow-moving or lower-margin inventory through targeted discounts can free up working capital. Even if these discounts reduce margins in the short term, they can provide the liquidity needed to invest in the products that will drive the most value during and after this tariff suspension window.

Lastly, it's a chance for brands to really think strategically about their product catalog and margin profile. Can you afford to move fewer units at higher margins if you raise prices or discount less? Can you create more days or weeks of coverage through better merchandising strategies? These are the questions that brands should be carefully asking themselves when assessing their working capital availability ahead of their next PO.

Investing heavily in inventory during this 90-day tariff suspension can put a significant strain on working capital. Brands that choose to maximize their inventory in anticipation of future demand might find themselves in a tight liquidity situation. This approach could lead to a scenario where solvency is pushed to its limits as brands pour their resources into stocking up. This creates a competitive and risky environment, where only the most financially agile and cashflow positive brands will thrive.

Moreover, this rush to secure inventory and freight space could lead to a sort-of bidding war, further driving up costs and squeezing margins. Brands will need to balance their need for inventory with their financial health, ensuring they don't overextend and jeopardize their long-term viability.

To navigate this period effectively, brands should keep a close eye on key freight cost indices like the Freightos Baltic Index (FBX). The FBX provides a real-time benchmark for global freight rates, giving brands insights into current and projected shipping costs. Recent data shows that freight rates have been on the rise due to increased demand and limited capacity, a trend likely to continue as more brands scramble to place orders during this tariff relief window.

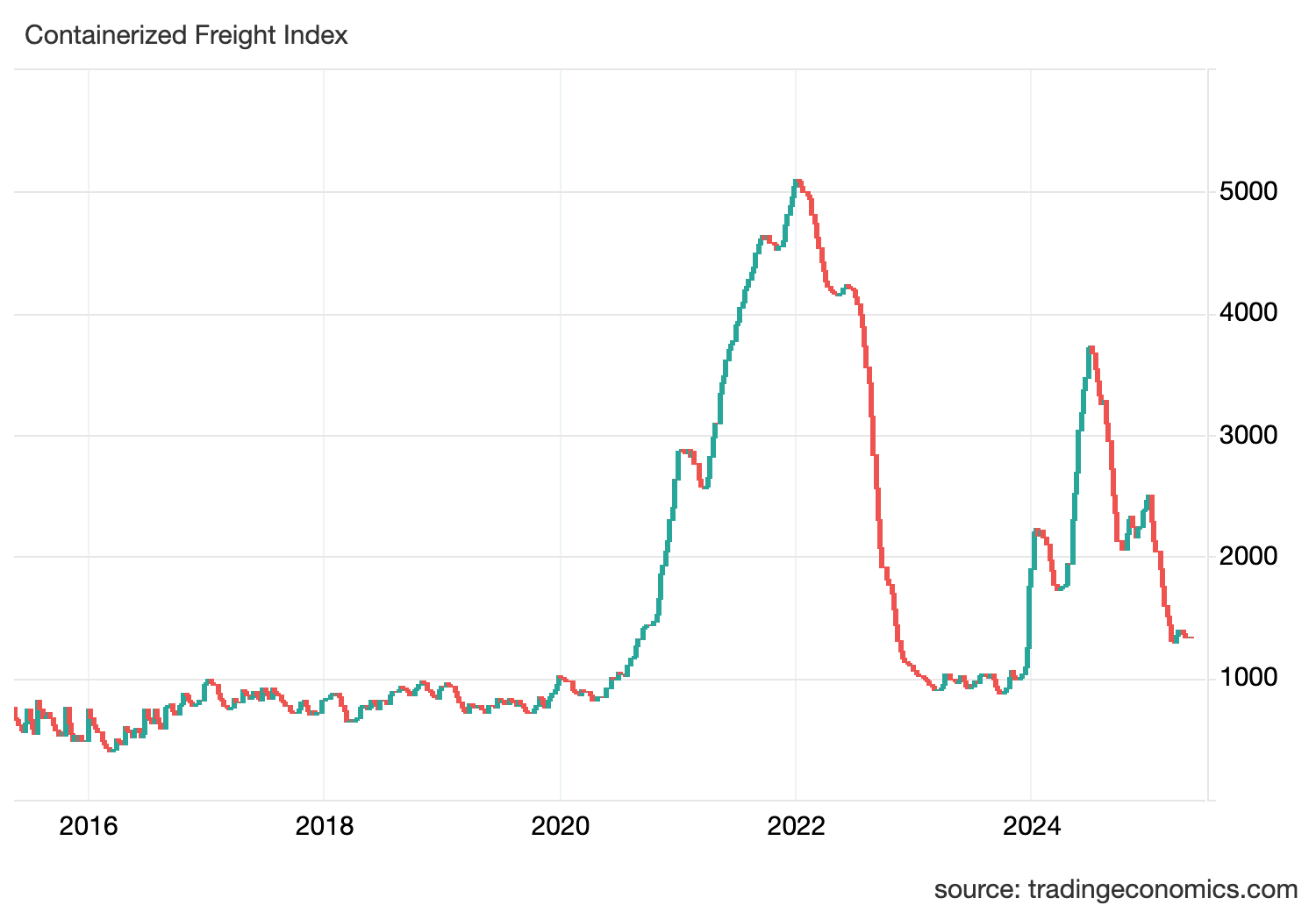

If we look at recent data from the Containerized Freight Index (CFI), we can see the precipitous decline in container demand YTD; this pattern is not uncommon in Q1 when we see a natural decline in freight demand, overlapping with seasonal consumer demand trends, as well as the impact of Chinese New Year on manufacturing.

If we examine the period between 2020-2023, we can see the drastic impact of the COVID-related supply shock on the CFI index, most notably in Q3 of 2021 and Q1 of 2022 when we recorded all time highs on the Index:

If we compare the CFI to the FBX chart by Freightos, we can see the same peak in freight prices from Q3 of 2021. While these were dramatic swings from peak to trough, it's still important to recognize that exogenous events such as the current tariff environment can lead to fundamental re-underwriting in prices across the supply chain.

When comparing these two charts, it's important to note that the peak price for containerized freight took place in Q3 of 2021 as recorded by FBX; however, the peak value of the CFI shows the index peaking in Q1 of 2022. This is because the CFI is also pricing in market sentiment and forward expectations in the form of futures contracts (CFDs) rather than spot prices on freight itself. This is why when we overlay the two charts you see a lagging effect between the Q3-21 and Q1-22 peaks on the two respective charts.

Over the past few weeks, the FBX has shown a noticeable uptick in shipping costs, particularly on key routes from China to the U.S. West Coast. This increase can be attributed to the rush of orders from companies looking to capitalize on the tariff suspension, coupled with ongoing supply chain constraints. For DTC brands, staying up to date on price movements is crucial for planning and budgeting. Understanding the trends in freight costs can help brands make informed decisions about when to place orders and how to manage their logistics budgets effectively.

As brands navigate this temporary tariff relief, the decisions they make now will have lasting impacts. The short-term relief from tariffs could be offset by increased freight costs, creating a new equilibrium that might not be as advantageous as it initially seems.

Despite the potential risk of freight costs increasing, the likely net effect of these reduced tariffs should still offer sizeable savings to merchants when comparing to the original 145% tariff plan put forward.

The likelihood of continued turbulence and tariffs should be priced into all brands financial models. DTC operators will need to be strategic, focusing on their core products and managing their working capital prudently to weather this period of uncertainty.

This temporary suspension offers brands a unique opportunity to reassess their supply chains and inventory strategies. By taking a measured approach—focusing on high-value inventory, maintaining financial flexibility, and staying nimble—brands can turn this period of uncertainty into a strategic advantage. The key will be to act swiftly but thoughtfully, ensuring that short-term gains do not compromise long-term stability.

Your partner is profitable growth.

+1 (249) 508 5889

info@aplogroup.com

1 Rideau St, Ottawa, ON. Canada K1N 8S7

Privacy Policy | Terms & Conditions

.svg)